What the government's annual report card omits, obscures, and attempts to spin and why it matters three days before the Union Budget.

I read economic documents for a living. Most of them are dry. Some are illuminating. A few are exercises in such elaborate self-congratulation that you have to admire the craftsmanship even as you despair at the content.

The Economic Survey 2025-26, tabled in Parliament today by Finance Minister Nirmala Sitharaman, belongs firmly in the third category. It proclaims India as the "fastest-growing major economy" for the fourth consecutive year. It celebrates 7.4% GDP growth. It positions us for a glorious march toward "Viksit Bharat 2047." The prose practically glows.

Now read the AICC Research Department's counter-document released alongside it, titled "Real State of the Economy 2026: Inequality on the Rise, Welfare in Retreat." Same country. Same data points. Two entirely different narratives.

One speaks of "macroeconomic resilience" and "structural transformation." The other documents systematic dismantling of rights, stagnating wages, and an economy where the top 10% now capture 58% of national income.

Which India is real? The answer lies not in choosing one narrative over another, but in examining what each chooses to highlight. And, more importantly, what it conveniently leaves behind in the shadows.

When Did the Economic Survey Become a Pamphlet?

Before we examine the contents, we need to acknowledge a structural problem that has been growing for years: the Economic Survey itself has changed beyond recognition.

This was once a document of sober economic analysis. It presented data. It acknowledged challenges. It offered evidence-based policy recommendations that sometimes contradicted the government of the day. Under Chief Economic Advisers like Kaushik Basu and Raghuram Rajan, the Survey maintained analytical distance. It questioned. It flagged risks. The 2013-14 Survey, for instance, included a frank discussion of why infrastructure projects were stalling and what structural reforms were actually needed, rather than merely celebrating announcements.

The Survey under Arvind Subramanian, while often innovative in its thematic choices, began to show greater alignment with government messaging. His "Surveys" introduced creative frameworks, such as the "JAM Trinity," and coined terms, including the "twin balance sheet problem," in the 2015-16 Survey. To his credit, the 2016-17 Survey included a careful analysis of the costs of demonetisation alongside the claimed benefits. But even Subramanian, after leaving office, publicly criticised India's GDP methodology, calling the numbers "mystifying" and noting they "don't add up." His willingness to speak truth after leaving office suggests the constraints he faced while in office.

The transition under Krishnamurthy Subramanian (2019-2022) marked a sharper turn. The Surveys began featuring more references to ancient Indian economic thought, more celebratory framing of government schemes, and less engagement with structural critiques. The 2020-21 Survey, released during the worst economic contraction since independence, somehow managed to frame the crisis primarily as an opportunity for reform rather than a failure of pandemic management. Independent analysis of GDP contraction was dismissed; the Survey's own estimates proved wildly optimistic compared to what eventually materialised.

The current iteration, under V. Anantha Nageswaran, completes the journey into promotional territory.

This year's Survey is saturated with references to "Viksit Bharat 2047," the government's political branding. It frames the VB-G RAM G Bill (the MGNREGA replacement) as a progressive reform "aligning rural employment with the Viksit Bharat 2047 vision." It does not examine what workers lose when rights become discretionary allocations. Special essays discuss "strategic resilience" and "strategic indispensability." These are terms that belong in political manifestos, not economic analysis.

The Wire documented this trajectory in its analysis of the 2022-23 Survey, noting how the document "handpicks only two periods in recent Indian economic history, the Vajpayee and Modi eras, in a bid to establish a 'right-wing economic trajectory.'" The UPA years, which delivered India's fastest wage growth and substantial poverty reduction, simply vanish from the comparative frame.

This is not accidental. It is foundational to the document's political purpose.

The Survey's increasing use of infographics over analysis, its celebration of scheme announcements over outcome assessments, and its consistent framing of challenges as "opportunities" all point to a document that has abandoned the pretence of independent economic assessment. This is dashboard governance at the national level: measuring what looks good rather than what matters. It has become what the government wants the economy to look like, not what it is.

This matters because the Survey was designed to serve a specific institutional function: to provide Parliament and citizens with an honest assessment of the state of the economy before budget allocations are made. When the document becomes an instrument of political marketing, that function collapses. We lose a critical feedback mechanism in democratic governance.

And that loss becomes particularly significant when the Union Budget arrives on 1 February.

The GDP Growth Story: When Numbers Don't Add Up

The Survey leads with its headline figure: 7.4% real GDP growth in FY26, with projections of 6.8-7.2% for FY27. CEA Nageswaran presented this with characteristic optimism, noting that India's "potential growth rate has risen to 7 per cent, up from 6.5 per cent three years ago."

Here's what the Survey glosses over.

The IMF's recent evaluation of India's national account statistics accorded it a C grade. This is a diplomatic way of saying the data has "shortcomings." A C grade places India's statistical reliability below most emerging economies. We are essentially asking investors and policymakers to trust numbers that the world's primary economic institution considers questionable.

The Survey's own figures show peculiar divergences. Manufacturing reportedly grew at 8.4% in H1 FY26. Yet the Index of Eight Core Industries (ICI), which comprises 40% of the Index of Industrial Production (IIP), grew by only 2.9% during the same period. How does booming manufacturing coexist with sluggish core industries?

Arvind Subramanian estimated that as much as 2.5 percentage points were overestimated in India's GDP. More recent analysis in Business Standard showed that discrepancies between production-side and expenditure-side GDP calculations ranged from 0% to 47% in 2024. Strip out statistical noise, and real growth momentum falls to approximately 4.1%.

The rupee tells its own story. It crossed ₹90 to the dollar in early 2026, having lost over 50% of its value since 2014. In 2025, it was among the worst-performing currencies in Asia. An economy "hitting a sweet spot," to use the Survey's language, does not typically see its currency in freefall.

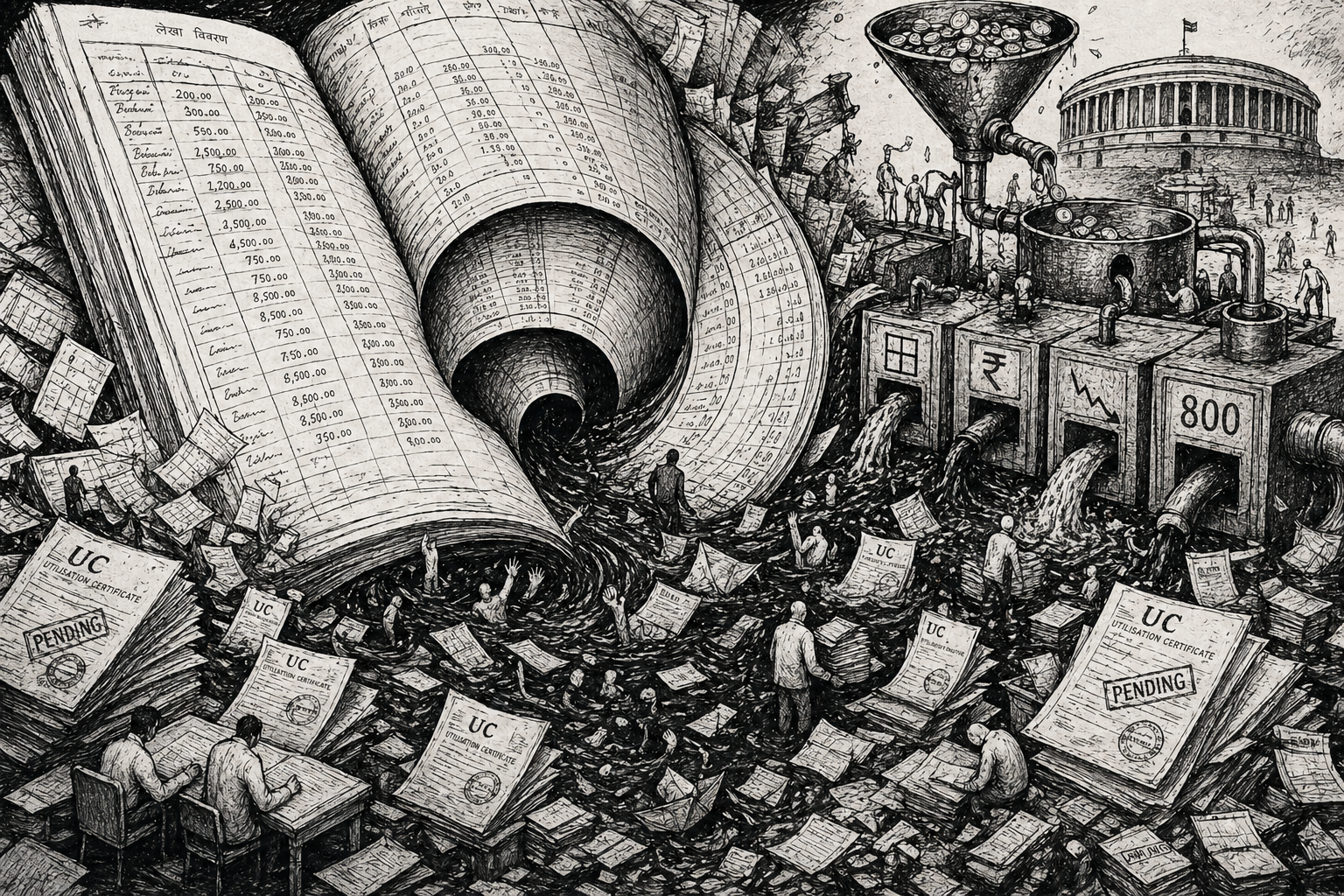

The Budget Numbers Nobody Talks About

Since the Survey sets the stage for Sunday's Budget, let's examine what the fiscal picture actually looks like.

The headline numbers sound responsible. Fiscal deficit targeted at 4.4% of GDP for FY26, down from 4.8% in FY25. Revenue deficit at 1.5% of GDP. Total expenditure of ₹50.65 lakh crore. Capital expenditure at ₹11.21 lakh crore, about 3.1% of GDP.

But look beneath the surface.

Interest payments now consume 25% of total government expenditure. That's ₹12.76 lakh crore going to service debt, not to build schools, hospitals, or rural roads. It is the single largest expenditure item in the Budget. More than defence. More than all welfare schemes combined.

In 2013-14, the last full UPA budget, interest payments consumed approximately 22% of total expenditure. A decade later, despite claims of fiscal prudence, that share has risen to 25%. In absolute terms, interest payments have more than tripled from around ₹4 lakh crore. This is the compounding cost of a decade of borrowing primarily to finance revenue deficits rather than productive investment. When the government borrows to pay salaries and subsidies rather than build assets, the debt becomes a permanent burden.

Here's the comparison that matters: interest payments now eat 37% of revenue receipts. For every rupee the government collects in tax, 37 paise goes to pay interest on past borrowings. This is a structural constraint that no amount of "Viksit Bharat" rhetoric can wish away. In the UPA's final year, this ratio was approximately 33%. We have moved backwards.

Social sector spending has collapsed as a share of the Budget. According to IDR's analysis, the social sector's share fell to an all-time low of 17% of total expenditure in FY25. Between 2014-15 and 2019-20, it averaged 21%. The government claims a rising economy; the budget allocations tell us the rising tide is not lifting all boats.

Consider the composition of this decline. Rural development allocations have fallen from 4.8% of total expenditure in 2013-14 to around 3.8% in FY26. The food subsidy, despite covering more beneficiaries on paper, has been compressed through administrative exclusions. Agriculture and allied activities have seen their share decline even as farm distress drives suicide statistics upward.

Centre-level health spending remains at approximately 0.3% of GDP, despite the National Health Policy target of 2.5% for total public health expenditure. The Ministry of Health allocation of ₹99,859 crore sounds large until you realise it's about ₹700 per Indian per year. For context, a single day in an ICU in a private hospital costs more than that.

MGNREGA allocation is frozen at ₹86,000 crore for yet another year. The government claims this shows the scheme is "less needed" because the economy is booming. The reality? With over ₹10,000 crore in pending arrears from last year, the effective new allocation is just ₹76,000 crore. And wages remain stuck at ₹289 per day while inflation has eaten away purchasing power.

The cesses and surcharges problem continues. As I've written in One Nation, Unequal Returns and The Arithmetic of Fiscal Centralisation, the Centre has increasingly relied on cesses and surcharges that are not shared with the states. In FY26, nearly ₹6 lakh crore will be collected through cesses and surcharges. States will see none of it.

The growth has been steady and deliberate. In 2013-14, cesses and surcharges constituted approximately 10% of gross tax revenue. By FY26, that share has risen to nearly 18%, with the absolute amount increasing from approximately ₹1 lakh crore to almost ₹6 lakh crore. Every rupee collected through cesses is a rupee that the states cannot claim as their constitutional share. When the Finance Commission recommends 41% devolution, the Centre responds by shifting more revenue into non-shareable categories.

The fiscal story the Survey tells is one of responsible management. The fiscal story the numbers mean is one of structural deterioration masked by accounting choices.

Employment: The Elephant the Survey Pretends to Ride

The Survey's treatment of employment constitutes a selective presentation. It celebrates "declining unemployment rates" and "improving employment conditions," notes the implementation of four Labour Codes and the recognition of gig workers, and frames the replacement of MGNREGA with VB-G RAM G as a progressive reform. Between 2017-18 and 2023-24, manufacturing's share of employment fell from 12.1% to 11.4%, services declined from 31.1% to 29.7%, and agriculture's share rose from 44.1% to 46.1%. Workers went back to farms.

This is not progress. It is a regression. It is the reversal of structural transformation that took decades to achieve. Workers are returning to farms not because agriculture is thriving, but because there are no factory jobs. As I documented in The Great Indian Migration Wave, the same regions have been exporting labour for 150 years. The pattern persists because the economy fails to create jobs in the communities where people live.

The granular data is worse. Nearly 58% of regular salaried workers have no written contract. More than half receive no paid leave or social security. The youth employment crisis indicates that 2.8 crore educated young people were actively unemployed in 2023-24. Another 10 crore, primarily women, have simply stopped looking for work. They've become "discouraged workers," a statistical category that is not counted as unemployed.

The gig economy, which the Survey celebrates as a new frontier of employment, warrants closer examination. The approximately 1.5 crore gig workers in India, delivering food and packages, driving cabs, and performing micro-tasks, have no severance, no healthcare, and no pension or performance benefits. The platforms that employ them classify them as "partners" to avoid labour law obligations. When the Survey cites "recognition" of gig workers under the Labour Codes, it does not mention that the actualisation of socio-gig workers' security provisions has been negligible. The e-Shram portal registered 30 crore informal workers; the benefits delivered to them remain minimal.

Women's labour force participation tells another story that the Survey prefers to obscure. The government celebrates the rise in female LFPR from 23% in 2017-18 to over 40% by 2023-24 as a success story. But examine the composition. This increase primarily reflects the greater inclusion of women in unpaid agricultural work on family farms and as domestic helpers, rather than entry into formal employment with wages and protections. The PLFS methodology classifies a woman who spends even a few hours helping on her husband's farm as "employed." When women exit the labour force entirely because caregiving burdens are incompatible with available jobs, they simply disappear from employment statistics. The economy does not count their absence as a failure.

The human cost? Between 2018 and 2023, 18,914 people died by suicide due to unemployment. In 2023 alone, 47,170 daily wage earners died by suicide. That's 28% of all suicides—the single largest occupational category.

The Survey mentions none of this.

MGNREGA's Death and the VB-G RAM G Deception

The Economic Survey presents the transition from MGNREGA to VB-G RAM G as a form of modernisation. The AICC report characterises it as the most significant rollback of social protection legislation in independent India. I've covered this in detail in In the Name of RAM: How India Just Dismantled Its Rural Safety Net.

Here's what changes under VB-G RAM G:

The 100-day work guarantee is reduced to "up to 125 days" at the state's discretion. The legal guarantee of work within 15 days disappears. The unemployment allowance for unmet demand vanishes—funding shifts from 100% Centre-borne to a 60:40 split with states.

The naming is deliberate. "G RAM G" echoes "Gram" while invoking the politically charged name of Ram. The Bill passed while Parliament was debating the anniversary of the Ayodhya consecration—symbolism doing the work of substance.

Between 2019 and 2025, 4.57 crore job cards were deleted from MGNREGA. The government frames this as "cleaning up ghost beneficiaries." But Aadhaar-linked verification systems were already in place. These deletions systematically excluded legitimate workers through technical failures, changed biometrics from manual labour, and bureaucratic attrition. Many workers found their cards deleted after their fingerprints, worn smooth by years of manual labour, no longer matched biometric records. Others lost access because they could not navigate the digital verification systems. The "cleaning" cleaned out the most vulnerable.

The shift in funding to a 60:40 Centre-state split is where the real damage lies. States already struggling with their own fiscal deficits, many of them caused by reduced central transfers and GST compensation gaps, will now bear an additional burden of ₹ 50,000 crore. Poorer states, which need the scheme most, are precisely the states least able to afford their new share. Bihar, Uttar Pradesh, Jharkhand, and Odisha, the states that supply the bulk of migrant labour because local employment is unavailable, will either cut programme provision or divert funds from other welfare schemes. The design ensures that the scheme will thrive where it is most needed.

The objective metric: Average days of employment per household peaked at 51 days in 2018-19, then fell to around 44 days by 2024-25. The scheme provided less work even as the need grew.

The Inequality the Survey Cannot Hide.

The Survey speaks of "poverty reduction" and "inclusive growth." The World Inequality Report 2026 presents a different picture. As I explored in Stock and Flow: Why India's Welfare State Cannot Touch Wealth, the government's approach smooths consumption flows while leaving the stock of Wealth entirely untouched.

India's top 1% now owns 40.1% of the national Wealth. The top 10% captures 57.7% of the national income. These are levels of concentration worse than during British colonial rule. The World Inequality Lab notes that this represents one of the most extreme wealth concentrations among major economies.

Let me make this concrete. Between 2014 and 2024, the combined Wealth of Indian billionaires grew from approximately $100 billion to $954 billion. That's nearly a tenfold increase. During the same period, real wages for agricultural workers grew by approximately 1.2% annually, barely keeping pace with inflation.

Or consider this: the Adani Group alone added Wealth equivalent to the combined GDP of several northeastern states during this period. One family. One decade.

The consumption data is just as damning. The 2023-24 Household Consumption Expenditure Survey (HCES) showed that the top 5% of urban households spend more than six times what the bottom 50% spends. In rural areas, the ratio is even more extreme. The average monthly per capita expenditure in rural India remains below ₹4,000 for the bottom half of households, while the urban top 5% exceeds ₹20,000. This is not a gap that "trickle-down" economics can bridge; it requires active redistribution that current policy explicitly rejects.

The regional disparities compound the picture. Per capita income in Goa is approximately ₹6 lakh per year, whereas in Bihar it is approximately ₹60,000. A tenfold difference between the richest and poorest states. The Survey celebrates national averages that mask these chasms. When the government reports "rising per capita income," it does not mention that the gains concentrate in a handful of states while the eastern belt from Bihar through Jharkhand to Odisha remains trapped. These are not just numbers; they represent the life chances of children born in different postcodes of the same country.

The distribution of the tax burden exacerbates this. Individual taxpayers now contribute more to the exchequer. The 2019 corporate tax cut, which reduced rates from 30% to 22% for existing companies and from 15% to 10% for new manufacturing units, cost the exchequer approximately ₹1.5 lakh crore annually. This was justified as an investment stimulus. Half a decade later, private investment remains stagnant relative to GDP, while corporate profits have soared. The Wealth created is relative to the shareholders rather than reinvested in capacity or jobs.

Meanwhile, 34% of India's population survives on less than ₹100 per day. That's 47 crore people. The Survey doesn't mention them.

Health and Education: The Missing Priorities

The Survey celebrates "improvements in human development indicators." The budget allocations tell a different story.

Health expenditure from the Centre at around 0.3% of GDP is approximately one-tenth of what the National Health Policy recommends for total public spending. As I wrote recently in When the IMF Speaks in Rupees, air pollution alone kills an estimated 20 lakh Indians annually, with economic losses exceeding 1.3% of GDP. The Survey mentions neither the deaths nor the economic cost. Even when state spending is included, total public health expenditure barely reaches 1.9% of GDP, remaining well short of the 2.5% target.

The numbers tell the story. India has approximately 0.7 allopathic doctors per 1,000 population, compared with the WHO recommendation of 1. The shortfall is worse in rural areas, compared with primary health centres remaining understaffed and under-equipped. Out-of-pocket health expenditure pushes an estimated 5.5 crore Indians into poverty every year; when a medical emergency strikes, families sell land, borrow at usurious rates, and deplete whatever savings they have accumulated.

The Ayushman Bharat scheme, widely celebrated in government communications, covers hospitalisation but not outpatient care. For Indians, the health burden comes not from rare hospitalisations but from the steady drain of medicines and consultations that consume household budgets month after month.

The scheme may have helped reduce catastrophic hospitalisation costs. Still, it has not solved the fundamental problem of a healthcare system that forces people experiencing poverty to choose between treatment and destitution.

The Ayushman Bharat Health Account, announced to create health IDs for all Indians, has recorded hundreds of registrations. However, the infrastructure of public health facilities remains under-resourced. You can have the world's most sophisticated health data system, and it will not compensate for hospitals without medicines, diagnostics without technicians, or primary health centres that open only three days a week because there is no staff.

Education fares no better. As I examined in The Education They're Building, years of defunding public Education have set the stage for privatisation. The Ministry of Education's allocation of ₹1.29 lakh crore represents 2.5% of the total Budget and about 0.4% of GDP. The National Education Policy recommends 6% of GDP. We are currently at one-fifteenth of that target.

The ground reality, as documented by ASER reports, shows that only 43% of Class 5 students in rural India can read a Class 2-level text. This has barely improved over a decade. The privatisation push has resulted in 61,923 government-aided schools closing between 2019 and 2023. The students from these schools do not vanish; they either transfer to government schools that are already strained beyond capacity or drop out entirely. The children who remain in government schools face teacher vacancies numbering in the lakhs nationwide, crumbling infrastructure, and a curriculum increasingly shaped by ideological priorities rather than learning outcomes.

Higher Education shows similar patterns. The gross enrollment ratio has improved, but the quality of Education in the thousands of new private colleges that have sprung up remains poor. Engineering colleges produce graduates that industry surveys consistently find unemployable. The National Education Policy promised increased public investment; the Budget delivers continued stagnation.

These are not economic statistics. These are children's futures being deliberately narrowed.

Manufacturing: The Make in India That Didn't

The Survey speaks of manufacturing revival and "China+1" opportunities. The data indicate failure, as documented in MSME Sector Under Siege: the decade since demonetisation has seen the steady destruction of small enterprises that were supposed to be the backbone of manufacturing employment.

Make in India was launched in 2014 with targets to increase the manufacturing share of GDP to 25% by 2022 and to create 100 million new jobs. A decade later, manufacturing's share has fallen from 16-17% to around 14%. Jobs in manufacturing have declined.

FDI tells the real story. Foreign Direct Investment into manufacturing fell by 43% between FY22 and FY24, from $16.3 billion to $9.3 billion. This was during a period when global investors were supposedly fleeing China for India. The China+1 narrative assumed that geopolitical tensions would automatically redirect supply chains toward India. In reality, Vietnam, Thailand, and Indonesia have captured most of the diverted investment. India's manufacturing ecosystem, hampered by poor infrastructure, inconsistent policies, and land acquisition challenges, was unable to capitalise on the opportunity.

The trade deficit with China has ballooned to $85 billion in FY24, widening further to $99 billion in FY25. We import Chinese components, assemble them with 6-8% value addition, and call it "Made in India." Apple iPhones assembled in India contain approximately $8-$10 of Indian value addition out of a $1,000 product.

Examine the Production Linked Incentive (PLI) schemes more closely. The government allocated ₹2 lakh crore across 14 sectors, with additional commitments to generate ₹30 lakh crore in production and 60 lakh new jobs over five years. The actual outcomes have fallen far short. As of late 2025, PLI disbursements totalled approximately ₹24,000 crore against claims of over ₹16 lakh crore in additional production. The production numbers sound impressive until you examine where the value is created. Most disbursements have gone to large corporations already operating in India, particularly in mobile phone assembly and pharmaceutical manufacturing.

The electronics sector illustrates the pattern. Mobile phone assembly has grown, but the domestic component manufacturing ecosystem has not developed. India's import bill for electronic components continues to rise. The phones are assembled here; the value is created elsewhere. The semiconductor PLI scheme, announced with great fanfare, has seen its primary investment proposals repeatedly delayed or scaled back. India remains entirely dependent on imports for chips.

The automobile sector, once a manufacturing success story, has seen employment decline even as production recovered post-pandemic. Automation and the shift toward electric vehicles, which have limited capacity among Indian companies, threaten further job losses. The Survey celebrates PLI approvals for automobile and drone manufacturing without examining whether the jobs promised will materialise.

For MSMEs, the picture is worse. Demonetisation in 2016, the chaotic GST implementation in 2017, and the pandemic lockdowns in 2020 delivered successive shocks that destroyed millions of small enterprises. Jobs in the organised sector did not replace these. The informal sector absorbed the displaced workers at lower wages and worse conditions. The formalisation drive, intended to bring workers into the tax net and social security system, has instead pushed them further into precarity.

The manufacturing story the Survey tells is one of resilience and opportunity. The manufacturing story suggested by the data is one of structural failure and unfulfilled promises.

The Methodological Problem

There's a deeper issue that the Survey does not address. The Periodic Labour Force Survey (PLFS) has undergone repeated structural changes, most recently in January 2025, thereby complicating historical comparisons. Under the PLFS methodology, India reports unemployment at 4-5%, partly because it counts unpaid family labour and subsistence work as employment. A woman working without pay on her husband's farm is "employed." A street vendor earning ₹50 a day is "employed." A Reuters poll found that more than 70% of independent economists believe India's official unemployment data are inaccurate. Alternative estimates range from 7% to 35%.

The Census remains frozen at 2011 data. We are making policy for 2026 based on population figures that are 15 years old. This means approximately 23 crore Indians added since then are not reflected in food security entitlements, electoral delimitation, or resource allocation. When your thermometer is broken, the temperature reading means nothing.

What Sunday's Budget Will Reveal

The Union Budget on 1 February will reveal what the government actually prioritises, rather than what it claims to prioritise. Watch for these indicators:

Will MGNREGA/VB-G RAM G allocation increase, or remain frozen while inflation erodes its value further?

Will health expenditure move toward the 2.5% of GDP target, or remain stuck at less than 2%?

Will the reliance on cesses and surcharges continue to grow, further centralising fiscal power away from states?

Will interest payments continue to consume a quarter of expenditure, thereby limiting budgetary space for other expenditures?

Will the benefits of the new tax regime flow primarily to the middle and upper classes, or will there be meaningful support for the 47 crore Indians surviving on ₹100 a day? * According to the World Bank's lower-middle-income poverty line ($4.20/day in 2021 PPP), approximately 24% of Indians, or 35 crore people, live below this threshold. Adjusted for inflation to current prices, this translates to roughly ₹100 per day.

The Survey has set expectations. The Budget will reveal reality.

What Must Be Done

The Survey isn't wrong that India has growth potential. But potential unrealised is just another word for failure. The path to a genuine Viksit Bharat requires confronting uncomfortable truths.

First, restore demand-driven rural employment guarantee. VB-G RAM G is a step backwards. Budget ceilings cannot ration rights. Second, publish credible, independently verified economic data. An IMF C-grade on statistics is a national embarrassment. Trust the numbers first; then ask others to trust them. Third, reverse the taxation tilt. When individuals pay more tax than corporations, and the super-rich add ₹2,000 crore (Oxfam's 2019 India Supplement reported Indian billionaire wealth growing by ₹2,200 crore daily. Given accelerated wealth accumulation documented in Oxfam's 2025 global report (₹2,000 crore represents a conservative current estimate), daily, while 28-30% survive on ₹100 a day, the system is broken.

Fourth, invest in health and Education. Less than 2% of GDP is spent on health, while air pollution kills 20 lakh people annually. Spending less is not a policy. It is negligence. Fifth, address market concentration. The Herfindahl-Hirschman Index (HHI) for Indian markets has risen to 2,532, indicating concerning concentration. Competition, not cronyism, drives innovation and keeps prices fair. Sixth, update the Census. Using 2011 population data in 2026 means approximately 23 crore Indians added since then are not reflected in food security entitlements, electoral delimitation, or resource allocation.

The Economic Survey 2025-26 is a document designed to reassure markets and justify upcoming budget allocations. That's its institutional purpose now. But it should not be mistaken for an honest assessment of the Indian economy.

To that end, we must examine the data it omits, the trends it downplays, and the lived experiences of the 80% of Indians surviving on less than ₹200 a day (based on the World Bank's Upper-Middle-Income Country (UMIC) poverty line of $8.30/day (2021 PPP), adjusted to approximately ₹200 in current prices. This benchmark reflects living standards in countries like China and Mexico. At this threshold, over 80% of Indians fall below the line). Their economy, the real state of the economy, awaits acknowledgement and action.

Sunday will tell us whether the government is listening.

Further Reading

Primary Sources

Economic Survey 2025-26 (Government of India): The official document tabled in Parliament. Read this to understand how the government frames its economic achievements and priorities.

Real State of the Economy 2026 (AICC Research Department): A comprehensive 104-page counter-document examining gaps between policy claims and ground reality. Covers GDP data quality, employment crisis, MGNREGA dismantling, inequality, health, Education, and manufacturing failures.

On Data Quality Concerns

IMF's data quality assessments of India's national accounts.

On the Survey's Transformation

"Three Reasons Why This Year's Economic Survey Is a Political Document" (The Wire, 2023): Documents the shift from economic analysis to political narrative.

On Budget and Fiscal Issues

PRS Legislative Research Budget Analysis: Comprehensive breakdown of budget allocations and trends.

IDR's analysis of social sector spending: Documents the decline in welfare allocations as a share of total expenditure.

On Specific Policy Areas

World Inequality Report 2026 (World Inequality Lab): Primary source for wealth concentration data showing top 10% capturing 58% of income.

ASER Reports: Ground-level data on educational outcomes vs. official claims.

Note: All statistics cited in this article have been cross-referenced with primary government sources, international agencies, and independent research. Where data conflicts exist, this has been noted.

Varna is a development economist and writes at policygrounds.press

Write a comment ...